Video je vhodné pre ŽIVNOSTNÍKOV, ZAMESTNANCOV aj ich KOMBINÁCIE.

Toto video každoročne aktualizujem – zapnite si titulky.

Vážim si ODBER na YouTube kanál, je to pre mňa podpora a signál, že sa vám páčia 🙂

Môžete ma podporiť symbolickým pozvaním na čaj cez IBAN: SK08 8360 5207 0042 0709 1593

Ďakujem za kliknutie na tlačidlo ODOBERAŤ na YouTube kanáli, cením si to 🙂

❤ Ste super! ❤

Pred vypĺňaním daňového priznania, odporúčam vo videu ZAPNÚŤ titulky a preletieť očami, všetky Aktualizácie nižšie

(zvlášť 7. a 9. Aktualizáciu):

Odkazy spomínané vo videu:

- Zistenie kódu SK NACE (jemne sa zmenila ale stále zadávate iba IČO)

► Kapitoly

0:00 Aký problém video rieši

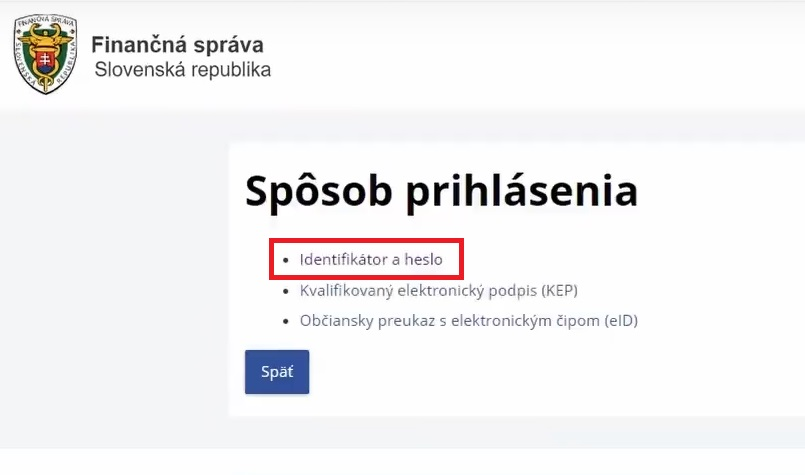

0:12 Prihlásenie sa do Finančnej správy

0:44 Nájdenie formulára Daňového priznania FO – typ B

1:25 Otvorenie formulára DP

1:39 Začatie vypĺňania DP

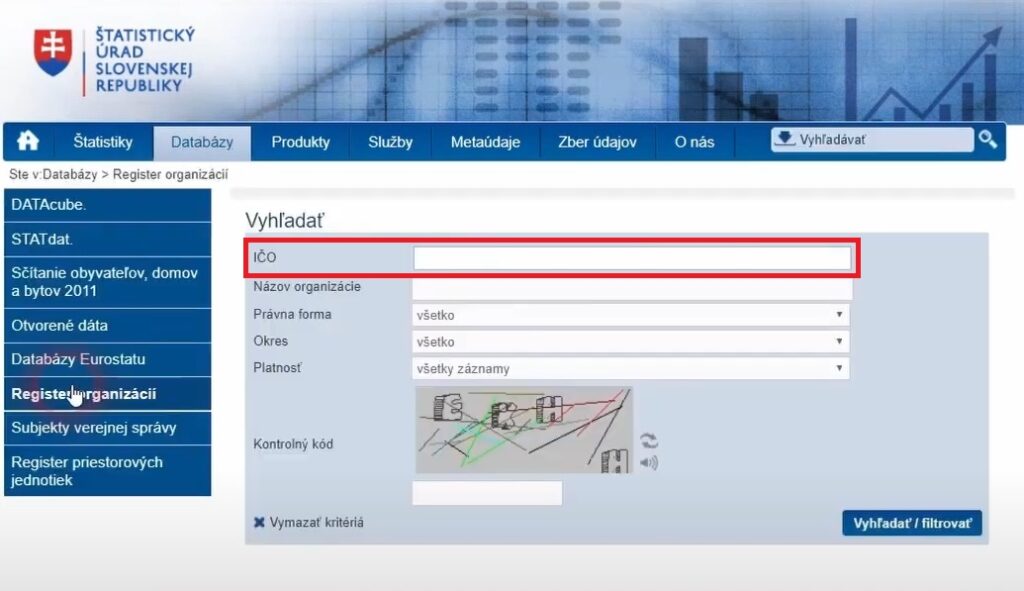

2:02 Zistenie SK NACE kódu

3:23 Vyplnenie SK NACE kódu

3:43 I. ODDIEL – ÚDAJE O DAŇOVNÍKOVI

3:53 III. ODDIEL – DAŇOVÝ BONUS (8. Aktualizácia)

4:04 V. ODDIEL – Príjmy od zamestnávateľov

5:01 VI. ODDIEL – Príjmy zo živnosti (z podnikania)

5:20 Príjmy z činnosti športovca

6:03 Uplatnenie si paušálnych výdavkov

6:16 Výdavky do zdravotnej poisťovne

6:36 Výdavky zo živnosti

7:20 Podmienky pre mikrodaňovníka (5. Aktualizácia)

7:31 Dvojkliky na automatické výpočty

7:55 IX. ODDIEL – III. pilier DDS (2. Aktualizácia)

8:19 Úhrn preddavkov na daň od zamestnávateľa

8:47 Daň na úhradu / Daňový preplatok (3. Aktualizácia)

9:02 XII. ODDIEL – darovanie 2% z dane

10:41 XIV. ODDIEL – Sociálne a zdravotné poistenie od zamestnávateľa

11:32 Odvody do zdravotnej poisťovne zo živnosti

11:58 Opravovanie chybových hlášok dvojklikom

13:29 Dvojitá kontrola cez tlačidlo Kontrolovať

13:59 XIV. ODDIEL – Vrátenie daňového preplatku

14:37 Nahratie prílohy (ak nemáte, neprikladáte nič)

15:39 Uloženie práce cez tlačidlo „Uložiť ako koncept“ (robte radšej priebežne – 7. Aktualizácia)

15:59 Podpísanie a podanie daňového priznania

0. Aktualizácia

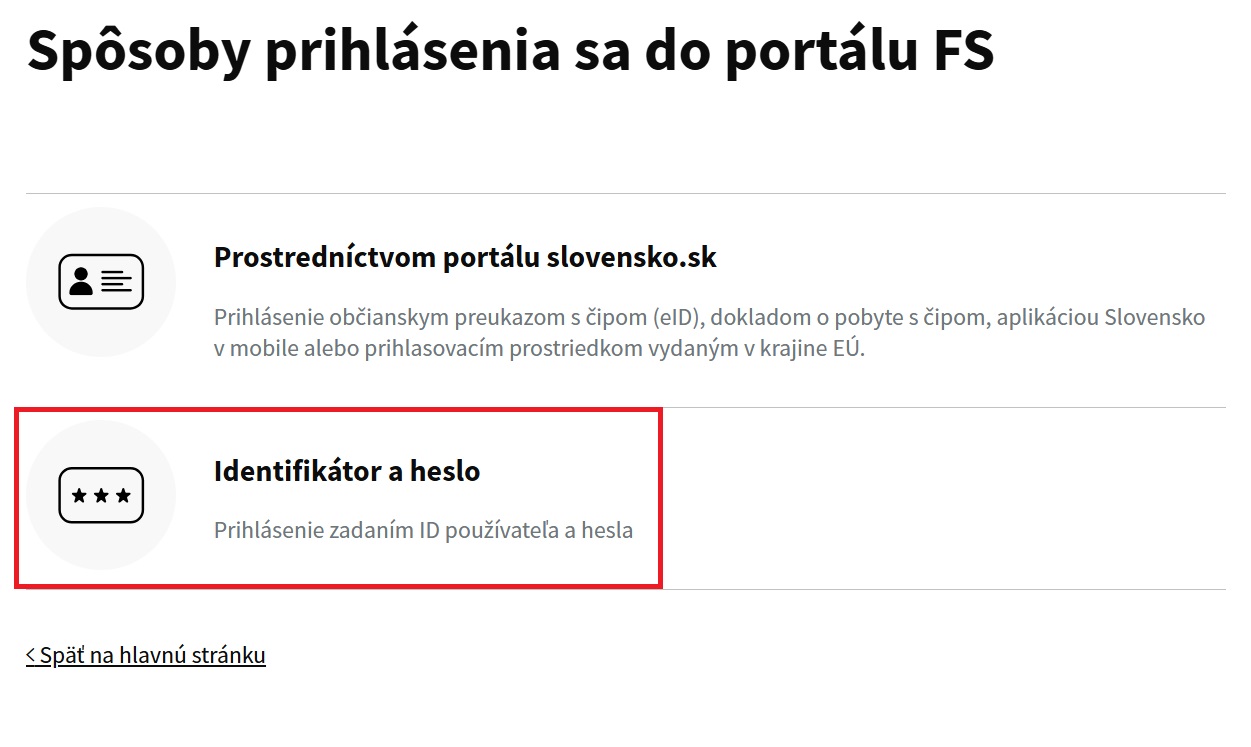

Prihlasovacie rozhranie sa (v čase 0:24) jemne zmenilo. Nám to však nevadí, lebo sa prihlasujeme cez Identifikátor a heslo. Môžete sa však prihlásiť aj cez portál slovensko.sk. Bude to fungovať.

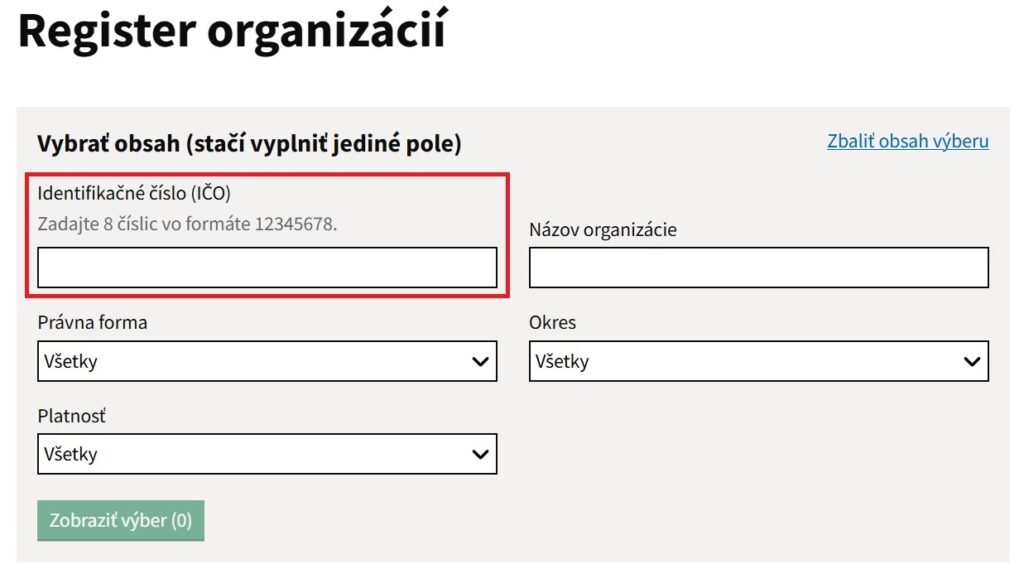

Tak isto Register organizácií sa jemne zmenil (v čase 2:35) ale funguje rovnako – stačí keď zadáte len vaše IČO – kliknete na tlačidlo „Zobraziť výber“ a potom už pokračujete ako vo videu v čase: 2:53 na zistenie vášho SK NACE kódu.

1. Aktualizácia

Tlačivo pre tento rok je takmer totožné, zmenilo sa iba niektoré číslovanie riadkov, ale ich obsah je rovnaký, iba majú niektoré riadky iné číslo :). Riaďte sa preto aj slovnými pomenovaniami riadkov, ktoré spomínam vo videu. Princíp aj spôsob vypĺňania je úplne rovnaký ako po minulé roky :). A samozrejme v katalógoch formulárov (ktoré spomínam v čase 1:15), si vyberiete aktuálne najnovšie daňové priznanie 🙂

2. Aktualizácia

Novinka, ktorá vo videu nebola spomenutá:

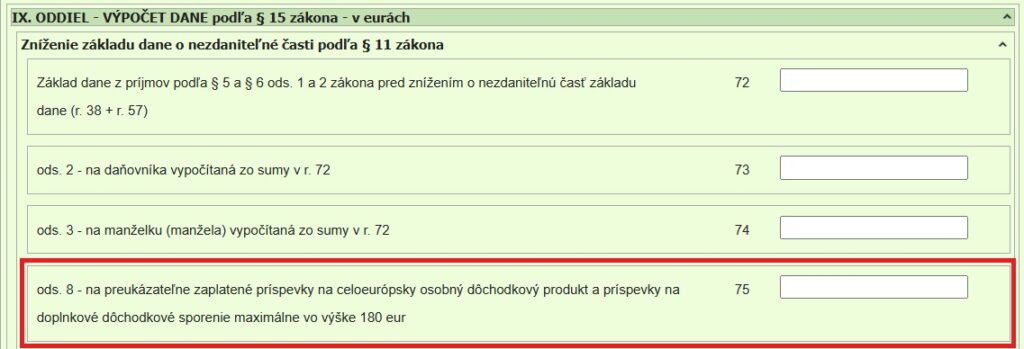

Môžete si uplatniť daňovú úľavu do výšky 180 €, ak máte III. pilier Doplnkového Dôchodkového Poistenia (DDS) otvorený po roku 2013* a ak vám zamestnávateľ zráža príspevky do tejto DDSky (teda ak vám do nej prispieva).

*Všetky DDS zmluvy, ktoré boli podpísané pred rokom 2013 nemajú nárok na uplatnenie daňovej úľavy. ALE. Pri prestupe (presune) do inej DDSky sa Vám môže zmluva rátať ako novo otvorená (teda už po roku 2013) a potom by ste mali získať nárok na uplatnenie si daňovej úľavy. Odporúčam si to pre istotu ešte overiť v DDSke, do ktorej by ste prestúpili. Ja som napr. prestupoval z TB DDS do NN DDS do Indexového fondu (ktorý odporúčam ak ešte nemáte 5 až 8 rokov do dôchodku) a všetko prebehlo v poriadku :).

– Toto číslo (sumu príspevkov do DDSky od vášho zamestnávateľa) získate z toho istého Potvrdenia o dani z príjmov (to jedno A4 PDFko), ktoré je spomínané aj vo videu (v čase 4:14), z riadku: 12 – Suma zamestnávateľom zrazených príspevkov na doplnkové dôchodkové sporenie: napríklad suma 123,45 € (aj keď bude vyššia, maximálne si môžete z nej uplatniť iba 180 €)

– danú sumu napíšete do Daňového priznania v IX. ODDIELI – VÝPOČET DANE podľa § 15 zákona – do riadku 75 ods. 8 – na preukázateľne zaplatené príspevky na doplnkové dôchodkové sporenie maximálne vo výške 180 eur – riadok 75: 123,45 (to je naša príkladová suma, vy si napíšte vašu)

– čo vám zníži Daň na úhradu, prípadne dá úplne na nulu v riadku 135 – Daň na úhradu – v tom istom IX. ODDIELY (takže možno nebudete musieť platiť žiadnu daň 🙂 )

Treba však myslieť na to, že pri predčasnom výbere z vašej DDSky, by ste dané úľavy na dani museli spätne uhradiť v DP. Je to za to aby ste si peniaze na dôchodok nevyberali skôr (napríklad na dovolenku) ale aby ste ich použili na to, na čo sú určené = na dôchodok 🙂

3. Aktualizácia

Ak by vám vyšla nejaká daň na úhradu v riadku 135 – Daň na úhradu – v IX. ODDIELY, tak ju musíte uhradiť.

Postup A:

Po podaní daňového priznania, sa vám v menu (v ľavom dolnom rohu) objaví možnosť

– Vygenerovania platobného príkazu –

– ten si môžete stiahnuť v PDF, v ktorom je IBAN, variabilný symbol, suma z daňového priznania a aj priamo QR kód na úhradu.

Postup B (v prípade nefungovania Postupu A):

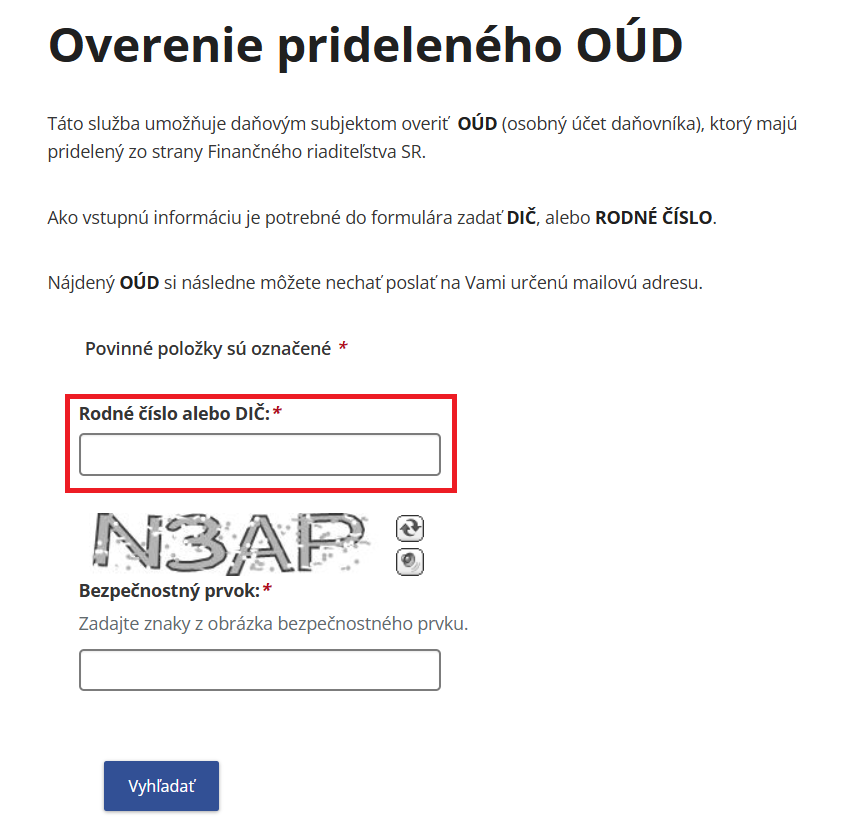

Ak neviete kde a na aký IBAN účet uhradiť daň, potrebujete najskôr zistiť vaše číslo daňovníka

– Vaše číslo daňovníka (osobný účet daňovníka = OÚD) zistíte po zadaní vášho rodného čísla alebo DIČ, na stránke finančnej správy: overenie prideleného OÚD – toto číslo (malo by začínať číslom 8…) si skopírujte

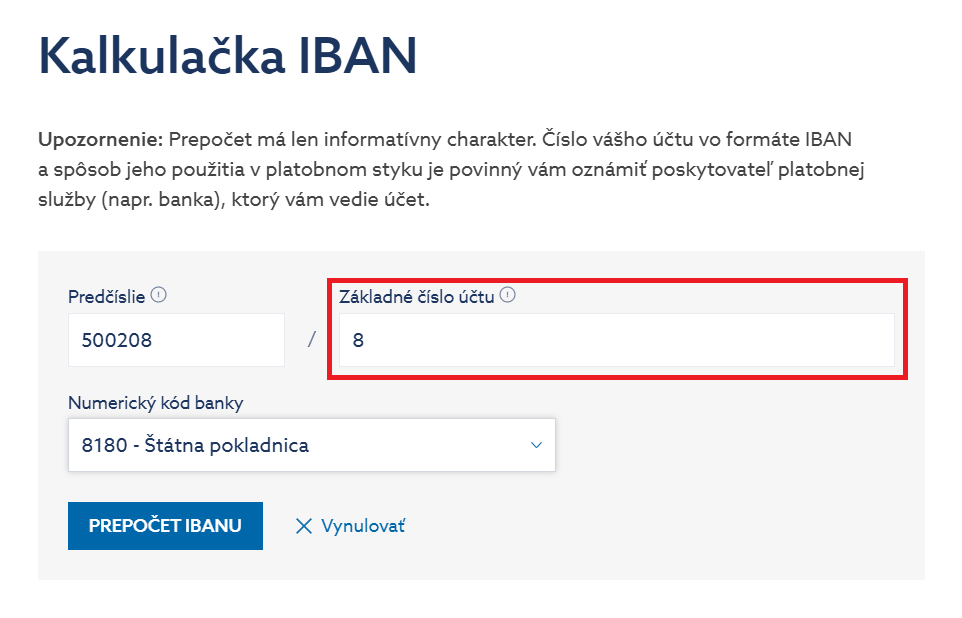

– teraz ideme z vášho OÚD vytvoriť IBAN na stránke národnej banky: kalkulačka IBAN

– do nej postupne zadáte:

– Prvá časť čísla účtu – Predčíslie, má byť: 500208 – Druhá časť čísla účtu – Základné číslo účtu, tu má byť ten váš osobný účet daňovníka = OÚD (to číslo začínajúce 8…), ktoré ste zistili, zadaním vášho rodného čísla alebo DIČ v predchádzajúcom kroku, zo stránky vyššie: 8XXXXXXXX

– Numerický kód banky má byť: 8180 – Štátna pokladnica – následne kliknite na tlačidlo „Prepočet IBANu“ a to vám ukáže IBAN (číslo účtu na uhradenie vašej dane)

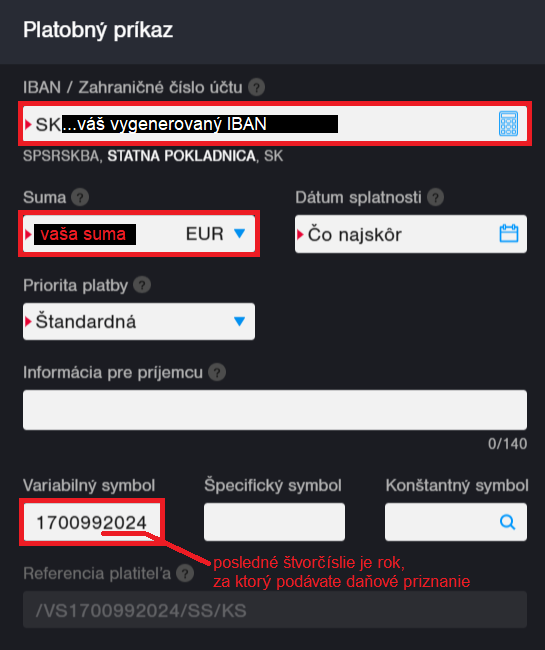

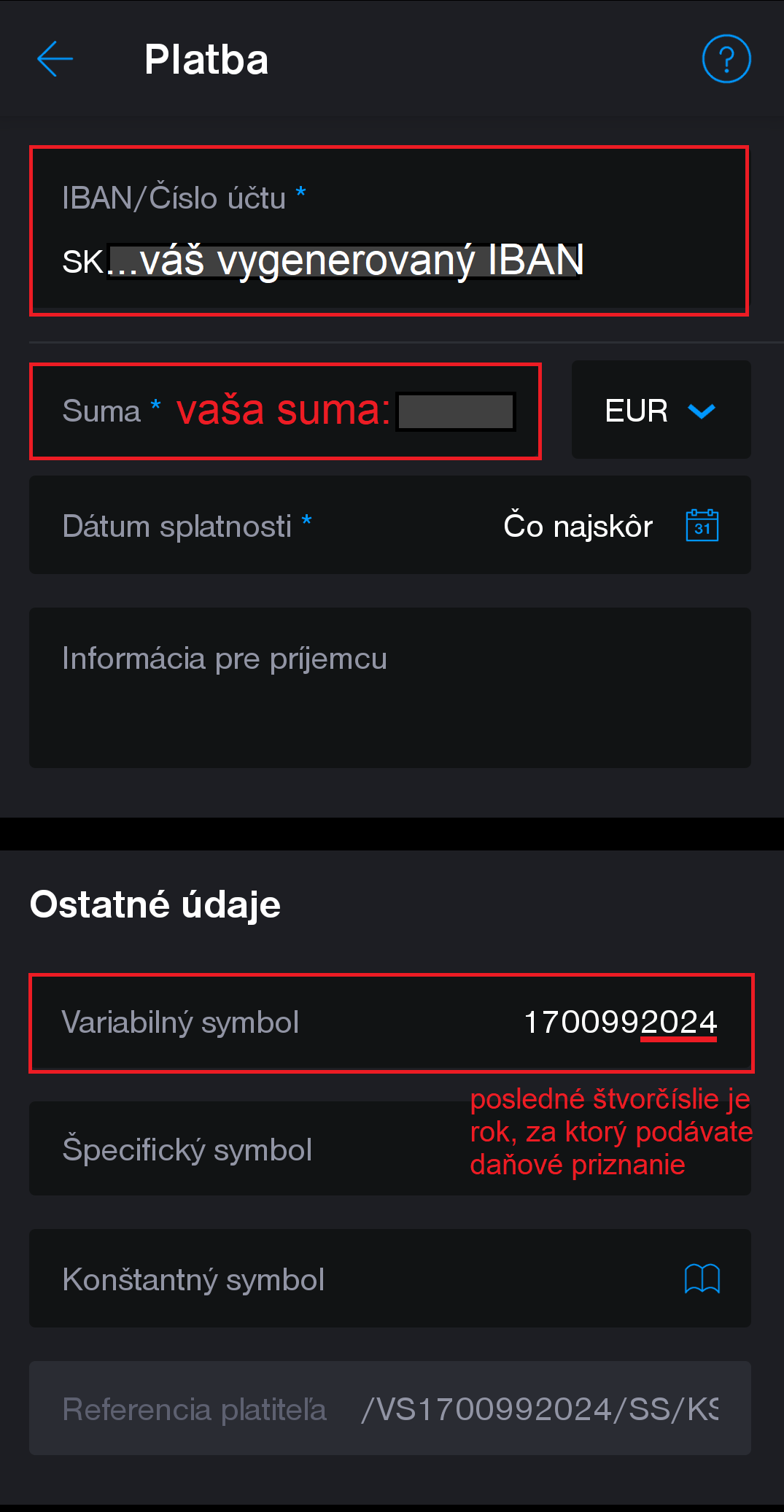

Následne budete okrem IBAN-u pri platbe potrebovať, zadať ešte variabilný symbol na úhradu dane.

– Ten je: 1700992024

– Posledné štvorčíslie „2024“ variabilného symbolu sa mení podľa toho za aký rok práve uhrádzate daňové priznanie.

– T.j. keď podávate daňové priznanie v roku 2025 za rok 2024, tak posledné štvorčíslie bude „2024“ 🙂

Platbu s uvedenými údajmi, môžete vykonať normálne v internet bankingu alebo cez aplikáciu vašej banky.

Príklady zadávania platobného príkazu cez Internet banking alebo cez mobilnú aplikáciu:

4. Aktualizácia

Ak vám vyjde nulová daň, tak v XII. ODDIELI – VYHLÁSENIE o poukázaní podielu zaplatenej dane

– označte políčko ✅ neuplatňujem postup podľa § 50 zákona

– Pretože máte nulovú daň a teda nemáte z čoho darovať 2 % nejakej neziskovej organizácii

5. Aktualizácia

Ak spĺňate podmienky pre mikrodaňovníka

– t.j. ste fyzická osoba a vaše príjmy (výnosy) z podnikania za zdaňovacie obdobie neprevyšujú sumu 60 000 eur,

– označte si v VI. ODDIELI – VÝPOČET ZÁKLADU DANE políčko ✅ Spĺňam podmienky pre mikrodaňovníka podľa § 2 písmeno w)…

6. Aktualizácia

Ak máte hypotéku, pri jej žiadaní ste mali max 35 rokov a za minulý rok ste priemerne za mesiac nezarábali viac ako 2 438,40 eur v hrubom (1,6 násobok priemernej hrubej mzdy – ktorá bola za rok 2024: 1 524 eur), môžete si uplatniť Daňový Bonus (DB) vo výške 50 % zo zaplatených úrokov v IV. ODDIELI – ÚDAJE NA UPLATNENIE DAŇOVÉHO BONUSU NA ZAPLATENÉ ÚROKY

– ak neviete aký bol váš priemerný mesačný príjem, vypočítate si ho, ako jednu dvanástinu zo súčtu všetkých vašich zdaniteľných príjmov (vaše faktúry a aj vašu mesačnú hrubú mzdu, ak ste boli popri živnosti aj zamestnaný)

teda: zdaniteľné príjmy ÷ 12 = váš priemerný mesačný príjem. A ak vám vyjde nižšia suma ako 2 438,40 eur, máte nárok na daňový bonus:

– označte si políčko ✅ uplatňujem daňový bonus na zaplatené úroky podľa § 33a

– vypíšte zvyšné políčka: Zaplatené úroky za zdaňovacie obdobie (v eurách), Počet mesiacov a Dátum začatia úročenia úveru

– môžete získať daňový bonus až do výšky maximálne 1 200 eur (za rok 2023 to bolo max. 400 eur)

– a od banky si požiadajte potvrdenie o zaplatených úrokoch za hypotéku (jedna A4), ktoré priložíte do príloh do DP (ešte pred jeho podaním)

7. Aktualizácia

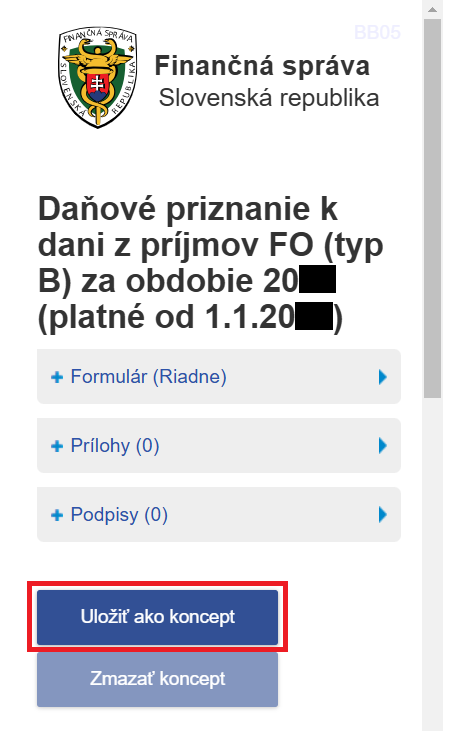

Priebežne si ukladajte rozpracované DP cez tlačidlo: „Uložiť ako koncept“. – Odporúčam to robiť už od začiatku vypĺňania DP.

Nájdete ho v ľavom menu hneď ako prvé tlačidlo:

Ak vám nefunguje uloženie rozpracovaného DP cez tlačidlo „Uložiť ako koncept“ (v čase 15:39) niekedy to zvykne urobiť pri dlhšom čase vypĺňania a vypíše vám chybu „token je neplatný“

– Dá sa tomu predísť priebežným ukladaním cez tlačidlo „Uložiť ako koncept“ (kým ešte token funguje) môžete to robiť koľkokrát chcete počas práce. Dôrazne to odporúčam.

– Ale pokiaľ už ste vyplnili kompletne DP a teraz si ho chcete pred podaním Uložiť ako koncept a vypíše vám chybu (mne to spravilo minulý rok tiež), dá sa to zachrániť tak (aby ste nemuseli všetko vypĺňať odznova):

– že si DP uložíte do súboru, cez tlačidlo „Uložiť do súboru“ v ľavom menu

– DP sa vám uloží do súboru s názvom output.xml do počítača (pravdepodobne do stiahnutých súborov),

– následne webovú stránku s DP obnovte/refreshnite (nebojte uložili ste si všetku prácu na DP do súboru output.xml vo vašom PC) možno si stránka vypýta opätovné prihlásenie, pokojne sa prihláste je to v poriadku,

– po obnovení a načítaní stránky s DP na ľavej strane kliknite na tlačidlo „Načítať zo súboru“

– stránka sa vás opýta – kliknete na Áno

– potom vo vybehnutom okne označíte súbor „output.xml“, ktorý ste si práve stiahli – a stlačíte Otvoriť,

– následne sa vám už krásne načítajú všetky predchádzajúce údaje, ktoré ste vypĺňali (takže to nebudete musieť všetko vypĺňať odznova) 🙂

Potom si budete môcť hneď kliknúť na tlačidlo „Uložiť ako koncept“ (pre istotu aj skontrolovať cez tlačidlo „Kontrolovať“ ktoré ukazujem v čase 13:34) a keď bude všetko OK aj podať cez tlačidlo „Podpísať a podať EZ-ou“

8. Aktualizácia

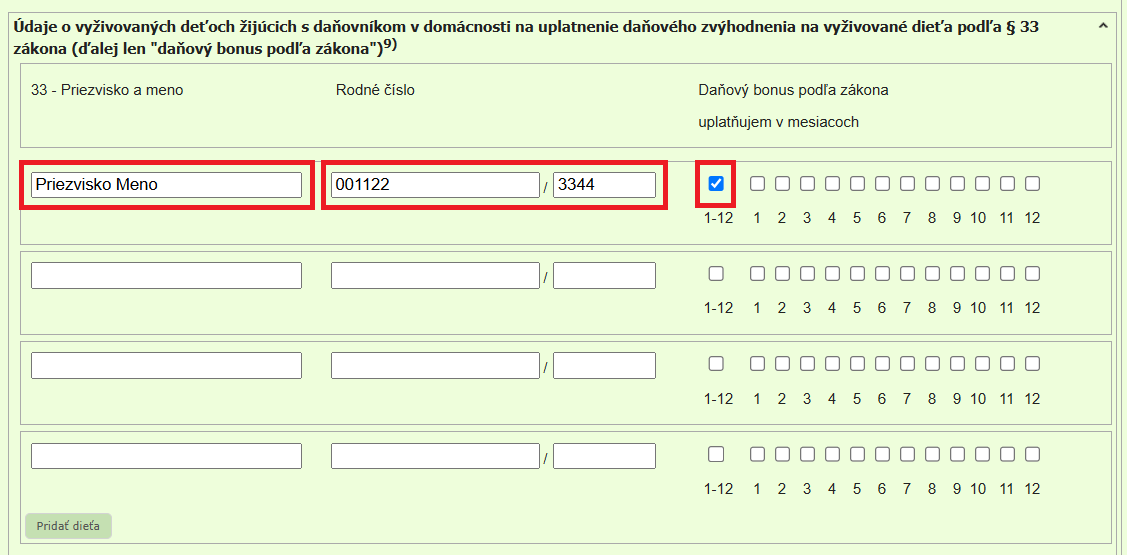

Ak máte deti, s ktorými žijete v spoločnej domácnosti (vyživované vami), majú do 26 rokov a sú študentmi denného štúdia, máte nárok na daňový bonus.

– choďte na III. ODDIEL – ÚDAJE NA UPLATNENIE ZNÍŽENIA ZÁKLADU DANE A DAŇOVÉHO BONUSU (ukázaný v čase 3:56)

– prejdite nižšie na riadok Údaje o vyživovaných deťoch žijúcich s daňovníkom v domácnosti…

– a do zobrazených okienok vypíšte údaje o dieťati/deťoch po jednom: Priezvisko a meno, rodné číslo a v políčkach ✅ označte počet mesiacov, počas ktorých vám náleží daňový bonus na dieťa (väčšinou to je celý rok t.j. 12 mesiacov, takže stačí označiť políčko 1-12, ktoré vám označí všetky políčka = celý rok)

9. Aktualizácia

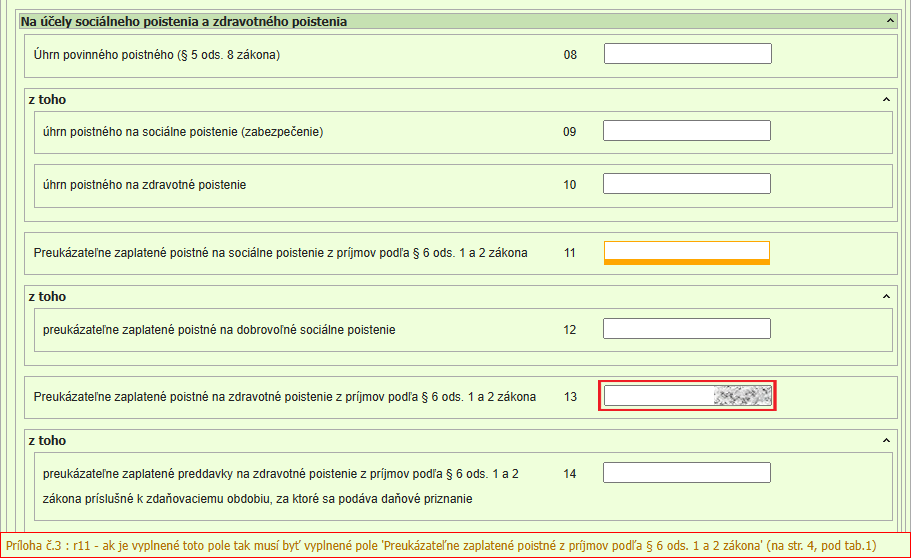

Ak ste IBA ŽIVNOSTNÍK (nie popri tom aj zamestnaný) a nemusíte platiť ešte sociálne odvody

– Úplne dole v XIV. ODDIELI v prílohe č. 3 – Na účely sociálneho poistenia a zdravotného poistenia – VYPĹŇATE IBA RIADOK 13 (výdavky na zdravotku) a všetky ostatné nechajte prázdne. V riadku 11 vám môže ukázať oranžovú chybu – nepíšte tam nič. (bola to logická chyba v tlačive ale už by mala byť odstránená – 13.01. 2025).

Ale ak vám dole oranžovým písmom ukazuje už iba túto jednu chybu (a po kliknutí na tlačidlo „Kontrolovať“ vám píše, že dokument obsahuje logické chyby), je to v poriadku, tie nebránia v odoslaní Daňového priznania a môžete ho podať. Opakujem toto platí, len pre tých, čo ešte neplatia sociálne odvody a nie sú popri živnosti aj zamestnaný. Všetci ostatný vypĺňajú a postupujú tak, ako je uvedené vo videu.

PS.: Keďže som viackrát dostával otázku na prikladanie faktúr do príloh, tak odpoveď je, že: do príloh neprikladáme žiadne faktúry. 🙂

Keby ste mali ešte nejaké dodatočné otázky, pokojne sa pýtajte v komentároch vo videu na YouTube alebo priamo tu dole na stránke 🙂

Môžete ma podporiť symbolickým pozvaním na čaj 🍵 cez IBAN: SK08 8360 5207 0042 0709 1593

alebo naskenovaním QR kódu:

Ďakujem za podporu 🙂 Veľmi si to vážim a cením 💚.